U.S. Grid Vulnerability in the AI Era

The artificial intelligence revolution runs on electricity. Every model trained, every query answered, every inference served draws power from a physical grid that was built for a different era – one of steady, predictable demand and decades of flat growth.

That era is over. Between 2023 and 2030, U.S. electricity demand is projected to nearly triple, driven overwhelmingly by the explosive proliferation of AI data centers. Yet the grid those data centers depend upon was largely constructed in the 1950s and 1960s. The mismatch between surging demand and aging, under-invested infrastructure is not a future problem. It is happening now.

This report examines three compounding dimensions of that risk: structural vulnerability in an aging grid, operational fragility rooted in the physics of electricity itself, and an emerging geopolitical threat that has already turned cloud infrastructure into a target. Together, these three layers define what may become one of the most consequential and underpriced systemic risks of the next decade.

01. The Foundation: How the U.S. Grid Works

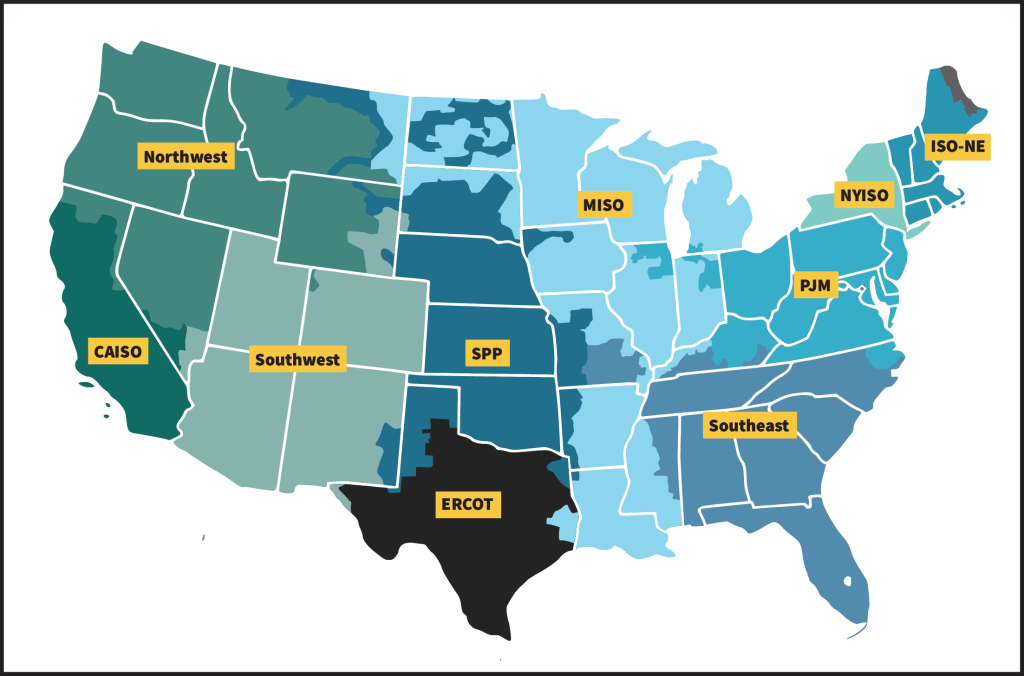

Before assessing what could go wrong, it helps to understand how the system actually functions. The U.S. power grid is not a single unified network. It is a patchwork of interconnected regional systems, each managed by a Regional Transmission Organization (RTO) or Independent System Operator (ISO). These entities are responsible for balancing supply and demand within their geographic footprints and overseeing transmission infrastructure.

The most consequential of these regions, for purposes of this analysis, is PJM Interconnection – the RTO covering Pennsylvania, New Jersey, Maryland, Ohio, West Virginia, North Carolina, and surrounding states. PJM is the sole authorized transmission provider for its region and, as we will see, the epicenter of the emerging power crisis.

02. The Demand Shock: 30 Years of Flat Growth, Then a Cliff

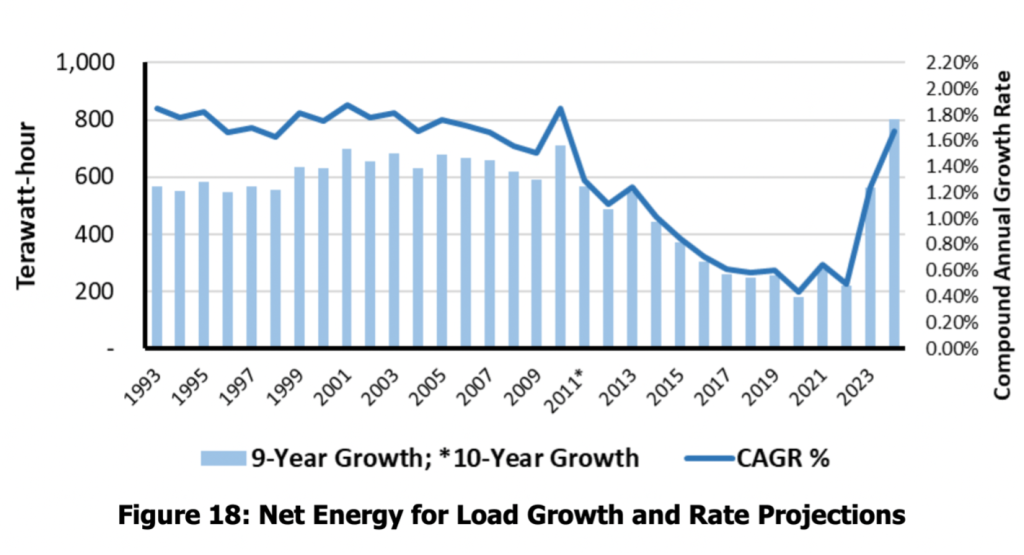

For roughly three decades – from the early 1990s through 2022 – U.S. electricity demand was essentially flat or gently declining. Gains in energy efficiency, the shift toward a service-based economy, and the offshoring of energy-intensive manufacturing all combined to reduce the load on the grid even as GDP grew substantially.

Grid operators and infrastructure investors adapted to this reality. With demand flat, there was little economic incentive to invest in major capacity expansion. New generation came online, but the pace of infrastructure buildout was calibrated to a world of modest, predictable demand growth.

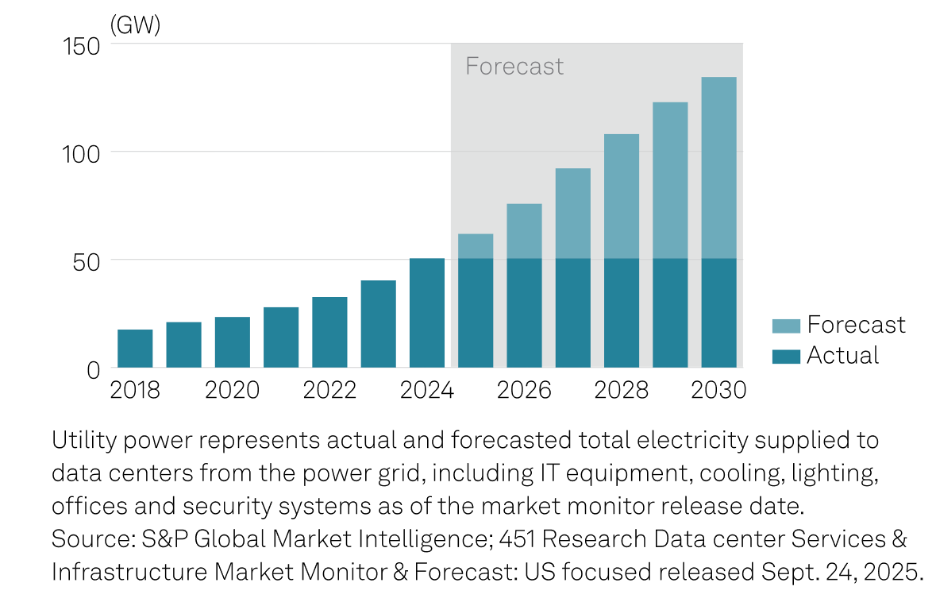

Then, beginning in 2022 and accelerating sharply through 2023 and 2024, demand spiked in a way that the industry had not seen in a generation. The primary driver: data centers, and specifically the massive computational infrastructure required to train and run large AI models.

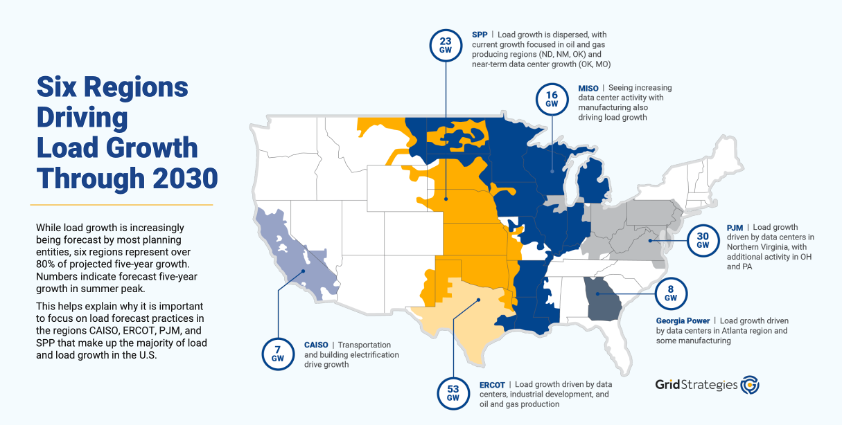

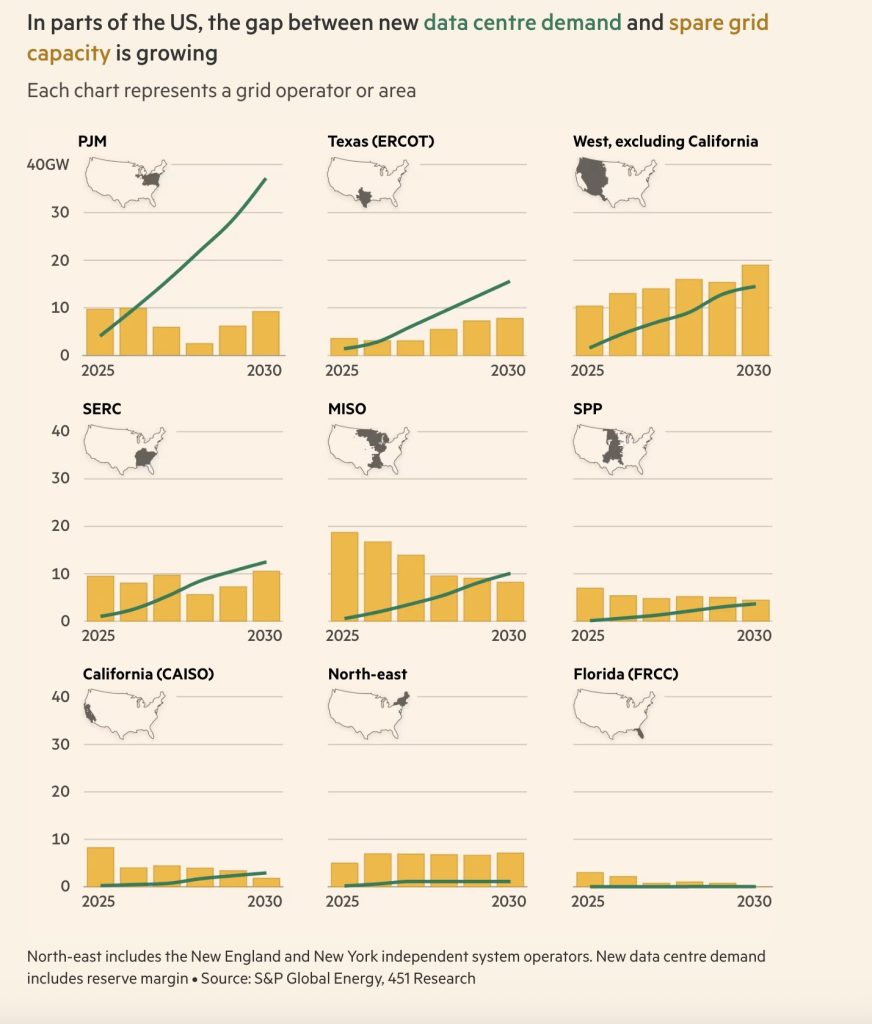

According to forecasts from Grid Strategies and S&P Global / 451 Research, demand growth through 2030 is uneven across the country. It remains manageable in the West and Midwest. But in Texas – and especially in the PJM region – the growth trajectory is extraordinary. The grid is being asked to absorb demand growth that would have seemed implausible just five years ago.

03. The Infrastructure Gap: A 1960s Grid Carrying 2030 Demand

The demand shock would be challenging even for a modern, well-maintained grid. But the U.S. grid is neither. The electrical infrastructure that powers the country was largely built between the 1950s and 1970s – designed for the demand profile of that era, with an expected service life measured in decades, not indefinitely.

During the long period of flat demand growth, RTOs had little financial or regulatory incentive to invest aggressively in infrastructure renewal. Maintenance continued, but large-scale replacement and expansion did not. The result is a grid that is simultaneously old and structurally under-built – now being asked to handle demand loads it was never engineered to carry.

| Indicator | Figure |

| Transmission lines over 25 years old | ~70% |

| Circuit breakers over 30 years old | ~60% |

| Power transformers over 25 years old | 25%+ |

| Average lead time to replace a large transformer | 12–24 months |

| PJM net capacity additions vs. demand growth | Lowest of any major region |

The statistics above, drawn from a U.S. Department of Energy assessment, describe a system that is aging across every critical dimension simultaneously. What makes this particularly dangerous is the lead time problem: large power transformers, the backbone of transmission infrastructure, can take one to two years to manufacture and install. A single failure is not a short outage – it can create an extended window of vulnerability.

The Lead Time Problem

Unlike most industrial equipment, large power transformers are not stockpiled. They are custom-built, often overseas, and take 12 to 24 months to procure and install. A major transformer failure in a high-demand region does not produce a short outage. It can produce months of degraded capacity – with cascading consequences for every enterprise that depends on cloud services running through that corridor

04. The Concentration Problem: Why PJM Is the Epicenter

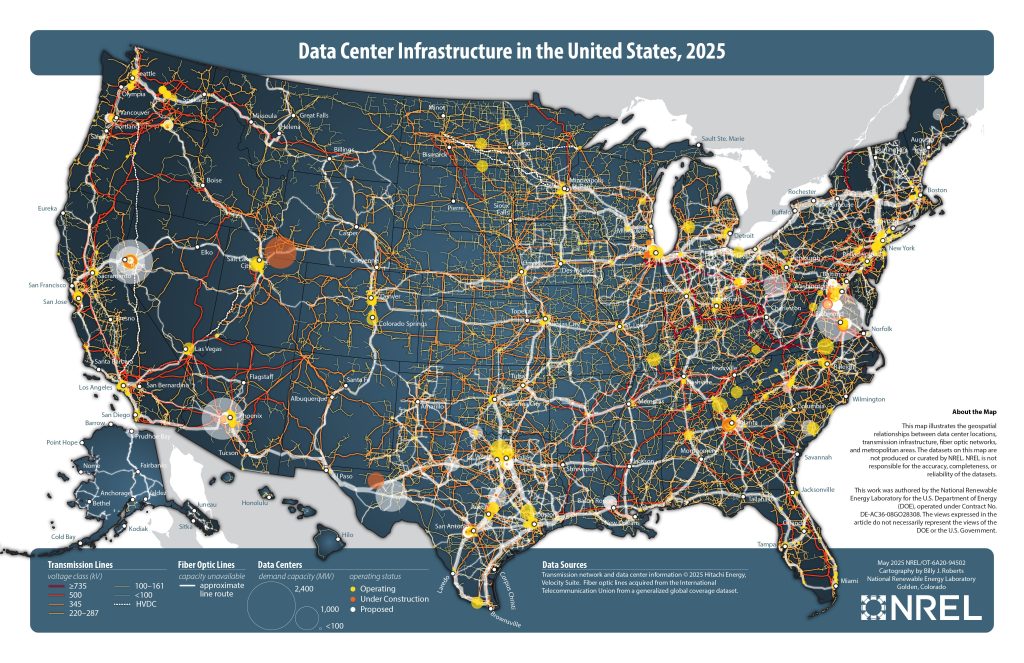

The structural vulnerability of an aging grid would be concerning anywhere. In the PJM region – and Northern Virginia in particular – it reaches a different order of magnitude.

Northern Virginia is home to the single largest concentration of data centers in the United States. Every major hyperscale cloud provider – Amazon Web Services, Microsoft Azure, Google Cloud, Meta, IBM – has built significant infrastructure there. The numbers reflect a concentration of digital dependency that has no equivalent anywhere in the world:

- 25% of all U.S. internet traffic routes through Northern Virginia

- The region hosts the greatest density of hyperscale data center capacity in the country

- PJM simultaneously has the lowest net additions to grid capacity of any major U.S. region

This creates what risk professionals would recognize as a single point of failure at systemic scale. Any enterprise that relies on cloud services – which, at this point, means most of the U.S. economy – has material exposure to what happens in this corridor.

Real-World Precedent – WSJ, March 2025

A single Virginia data center dropped off the PJM grid following a high-voltage line failure. The sudden loss of that facility’s massive power draw caused a destabilizing shock to the grid, forcing operators to rapidly shed generation capacity to rebalance supply and demand. That was one building. Northern Virginia has hundreds.

05. Three Layers of Vulnerability

To understand why this risk is so difficult to price – and so easy to underestimate – it helps to see it across three distinct but interconnected dimensions.

Layer 1 – Structural: An Old Grid, New Demand

The U.S. power grid was designed for steady, predictable demand. It was not designed for the load profile of AI-era data centers, which run at near-constant high capacity and are deeply sensitive to any interruption. Aging infrastructure – transformers, circuit breakers, transmission lines – creates failure points that would be manageable under normal conditions but become critical in a high-demand environment with little slack.

The core structural risk is not any single failure. It is that replacement timelines are measured in months or years, meaning one significant failure can leave a region operating in a degraded state for an extended period – exactly when demand is at its peak.

Layer 2 – Operational: Electricity Cannot Be Stored

Here is something most people outside the energy industry do not know: electricity cannot be stockpiled. Unlike oil, gas, or water, you cannot put electricity in a tank and draw it down later. It must be generated and consumed at the exact same moment – continuously, in near-perfect balance, across thousands of miles of interconnected lines.

Grid operators are walking a tightrope in real time, every second of every day. When the balance tips, it tips in one of two dangerous directions:

- Too much supply: A major data center campus goes offline unexpectedly. Too much electricity floods the grid, damaging generation equipment and potentially triggering cascading outages.

- Too much demand: Demand spikes beyond what supply can match. Grid frequency drops. Operators are forced to rapidly add generation – or forcibly disconnect customers to stabilize the system.

The March 2025 Virginia incident was a live demonstration of the second scenario. One facility going dark was enough to destabilize the regional grid. Extrapolate that to the full Northern Virginia corridor – 25% of all U.S. internet traffic – and the systemic implications become clear.

Layer 3 – Geopolitical: Data Centers as Strategic Targets

The third layer is the one most recently recognized by the risk community. Data centers are no longer merely commercial assets. They are large, visible, fixed, and increasingly strategic – making them attractive targets in a world where the boundaries between economic competition and geopolitical conflict are increasingly blurred.

The clearest illustration of this shift: several Amazon Web Services data centers in the Middle East sustained physical damage from drone strikes amid escalating regional conflict – marking the first confirmed instance of a U.S. hyperscale cloud provider being impacted by direct military action. The event demonstrated that the risk is no longer theoretical. Cloud infrastructure can be treated as a military target.

This transforms the risk calculus in a fundamental way. Physical attacks on data centers do not produce merely a local disruption. They produce – potentially – a systemic loss event with economic ripple effects that extend far beyond the affected facility.

06. Risk & Insurance Implications

The convergence of structural, operational, and geopolitical risk described in this report creates a set of insurance and risk management challenges that the industry is only beginning to grapple with.

Accumulation Exposure

The concentration of data center infrastructure in Northern Virginia creates a geographic accumulation exposure that has few historical analogues in commercial lines. A single triggering event – a major grid failure, a targeted physical attack, an extreme weather event – could produce correlated losses across hundreds of policyholders simultaneously. Traditional catastrophe models, built around natural peril footprints, are poorly calibrated for this kind of infrastructure-driven accumulation.

Business Interruption: Duration and Correlation

The lead-time problem for large transformers means that a major grid failure does not produce a short, bounded outage. It can produce months of degraded capacity – and months of business interruption losses that are difficult to model because they depend on equipment procurement timelines, regional grid configuration, and the specific failure mode. Policies written with standard waiting periods and duration assumptions may be materially underpriced for this risk.

Silent Physical Damage

As data centers increasingly become targets of physical attack – as demonstrated by the Middle East incidents – the boundary between cyber risk and physical damage risk becomes harder to define. A drone strike on a data center produces physical damage losses, but the downstream economic consequences propagate through digital infrastructure in ways that look like cyber losses. Risk professionals and underwriters need frameworks that can handle this blurring of peril boundaries.

Systemic Risk and Unmodeled Loss

Perhaps the most significant insurance implication is the one hardest to quantify: the possibility of a systemic loss event that exceeds any individual policy’s assumptions. If the Northern Virginia corridor experienced a major, extended outage – whether from grid failure, infrastructure attack, or compounding failures – the economic consequences would propagate through virtually every sector of the U.S. economy. This is not a risk that can be fully diversified. It requires scenario-based modeling, stress testing, and industry-wide coordination on exposure management.

07. Conclusion

The AI economy has a physical dependency that most risk models have not yet caught up with. Power is not an abstraction – it is the foundation on which every data center, every cloud service, every AI-driven business function rests. And that foundation is, in critical ways, fragile.

An aging grid, operating with almost no margin for error, now supports the most concentrated digital infrastructure in human history. That infrastructure is increasingly exposed to geopolitical threats that were not part of the risk landscape even five years ago. And the demand being placed on this system is growing faster than the system’s capacity to absorb it.

The question for risk professionals, underwriters, and policymakers is not whether a major power-related disruption will affect the AI infrastructure ecosystem. The structural conditions for such a disruption are already in place. The question is when it happens, how severe it is – and whether the risk community will have built the frameworks to respond before it does.

Sources & References

- NERC (North American Electric Reliability Corporation) – 2024 Long-Term Reliability Outlook

- Grid Strategies – U.S. Power Demand Forecast Report

- S&P Global / 451 Research – Data Center Power Demand Projections

- U.S. Department of Energy – Grid Infrastructure Assessment (2015)

- The Wall Street Journal – Virginia Data Center Grid Incident (March 1, 2025)

- PJM Interconnection – Regional Transmission Data and Capacity Reports